401 (k) plan is out of reach for small business? Maybe not anymore

Introduction

Small businesses have historically faced challenges in offering retirement plans to their employees due to the complexities and costs involved. According to the survey, about 74% of small business owners do not offer a retirement plan to their employees even though most employees need anywhere from 70-90% of their pre-retirement income to maintain their way of living after retirement.1

Though “Profits” is still considered to be the dominating reason for small employers to offering 401 (k) plan, the research published by the Employee Benefit Research Institute (EBRI), Center for Retirement Research at Boston College and Greenwald Research also found that even after all the national press coverage of SECURE and SECURE 2.0, most surveyed small business owners indicated they were not aware of the tax credits. Specifically, among the small business owners not offering a plan, nearly three-quarters (72%) of them said they were not aware of tax credits up to $5,000 being available to cover the costs of setting up a retirement plan. And 78% of them said the tax credits would make it at least somewhat more attractive to offer a plan.

Let’s take a closer look of the tax credits offered to small business owners:

- Credit Amount for setting up and administering a plan: The credit amount has been increased from the original SECURE Act. Eligible employers can now claim a tax credit of up to 100% of the costs incurred in setting up and administering a new 401(k) plan, up to a maximum of $5,000 per year for the first three years.

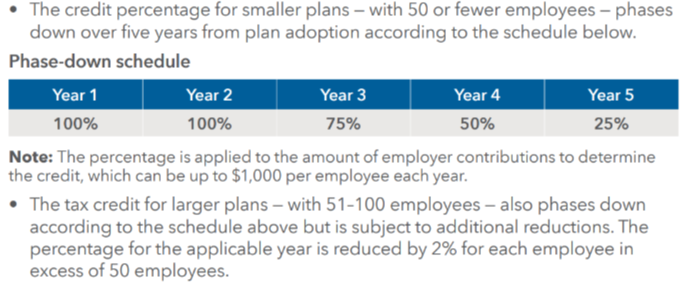

- Additional Credit for Employer Contributions: SECURE 2.0 also introduces an additional credit for small businesses that make employer contributions to their employees' retirement plans. This credit can cover up to $1,000 per employee, phasing out gradually over five years. Tax Credit Phase-down schedule for employer contribution:

- Startup Credit for Auto-Enrollment: If the new 401(k) plan includes an auto-enrollment feature, an additional tax credit of $500 per year is available for the first three years.

For Example: A Qualified employer, ABC company, has 12 employees, 10 of them making less than $100K, 9 of the 10 participate and each contributes $3,000 a year; employer match is 50%

1. Employer contributions:

50% × $3,000 employee contributions = $1,500 for each of 9 employees but capped at $1,000 each, so the total credit for 9 employees is $9,000. The total year 1 tax credit is $9,000, based on $13,500 of total employer contributions for 9 employees.

2. Plan costs: The Qualified employer pays annual plan costs of $4,500 and has 12 eligible employees, including 10 NHCEs

Credit calculation: $4,500 plan costs × 100% (fewer than 50 employees) = $4,500

Maximum credit: 10 NHCEs × $250 = $2,500

The total year 1 tax credit is $2,500 based on the maximum credit formula.

3. Automatic enrollment tax credit:

The credit is $500 per year for the first three years the feature is included.

If the employer received all credits, the tax credits for year 1 would total $12,000.

If you are one of the small business owners running a profitable business but with underfunded retirement assets, now is the time to learn about how SECURE 2.0 can help you set aside some of your business profits for retirement while taking care of your employee’s retirement.

The annual additions paid to a participant’s account cannot exceed the lesser of:

- 100% of the participant's compensation, or

- $69,000 ($76,500 including catch-up contributions) for 2024

For an age 50 owner, assuming was able to fund $76,500/year to a 401 (k) PSP, with 6% rate of return by age 60 he/she would have accumulated a million dollars for retirement.

If you are running a high profit professional organization (i.e. consultant, doctor, attorney, accountant…etc.) and would benefit from a much higher contribution range, there are other retirement plans that can potentially help to reach your goal.

Depending on each company’s individual situation, you may still be eligible to set up a 401 (k) plan for the year 2024. Please contact a qualified CEBS, pension consultant or attorney to find out.

Securities offered through Registered Representatives of Cambridge Investment Research Inc., a broker-dealer, member FINRA/SIPC. Advisory services through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Cambridge does not offer tax or legal advice. Cambridge and American Financial Alliance, Inc. are not affiliated.

Sources:

1) Forbes. “Should Your Small Business Offer a Retirement Plan?”

2) National Associates of Plan. “Small Biz Owners Seemingly Unaware of 401(k) Start-up Credits.”

3) IRS. “Retirement Topics - 401(k) and Profit-Sharing Plan Contribution Limit”